The Role of National Development Banks in the Climate Crisis

National development banks have a unique position in the fight against climate change. Their institutional design often allows them to take on greater risks, making them key players in driving sustainable development and supporting the climate transition.

To unlock this potential, these banks need access to incentivized funding sources—with costs aligned to profitable investments in decarbonization and environmental preservation and the mobilization of private capital.

How Do Development Banks Fund Their Operations?

Unlike commercial banks, most national development banks do not rely (or rely very little) on demand deposits. Instead, they raise resources through other mechanisms, forming their funding structure, which includes liabilities and equity.

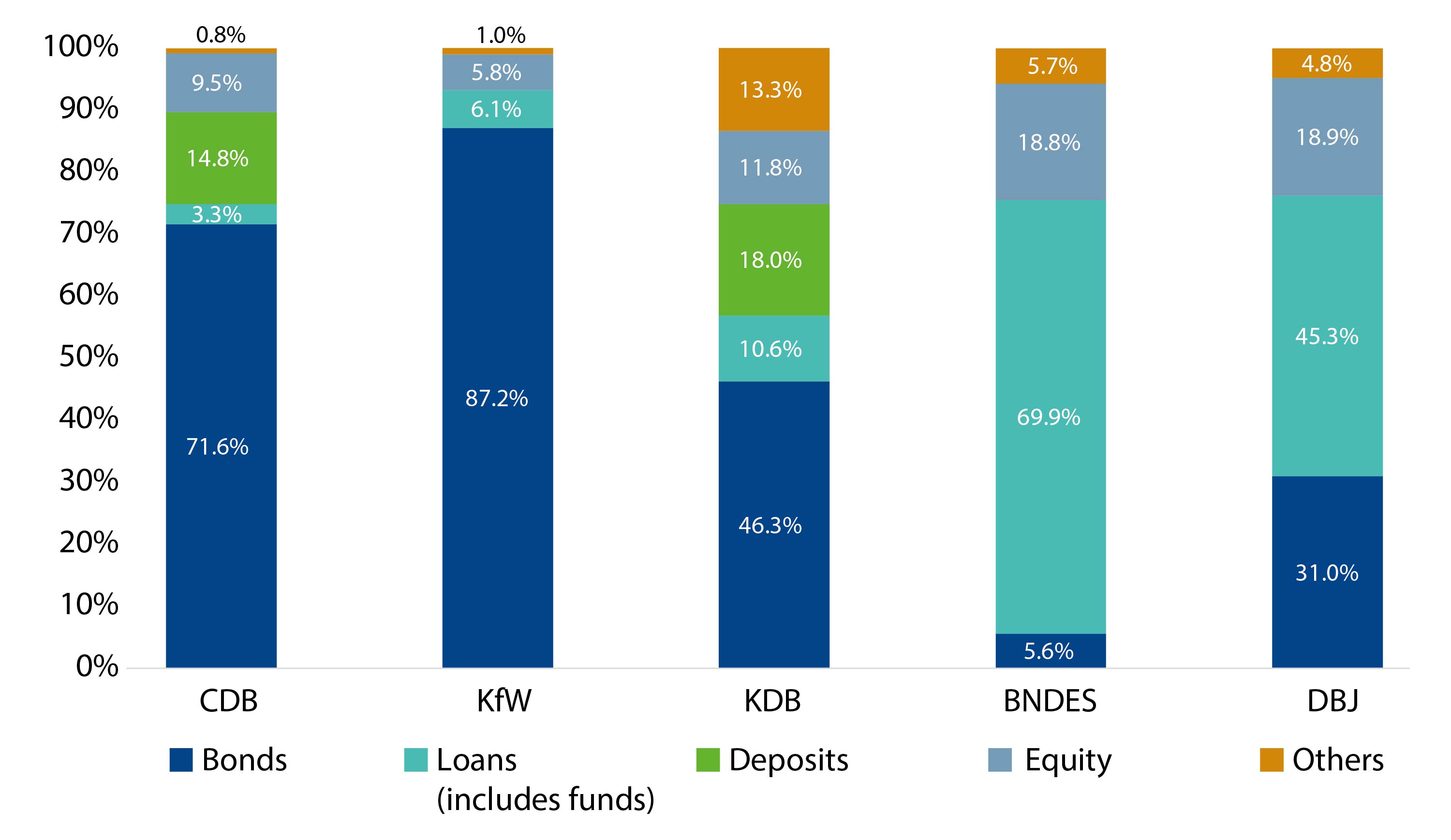

Composition of Funding for the Largest Development Banks (2024)

Source: Balance sheets from BNDES and DBJ.

CDB: China Development Bank; KfW: Kreditanstalt für Wiederaufbau; KDB: Korea Development Bank; DBJ: Development Bank of Japan.

Note: The French Caisse de Dépôt et Consignations and the Italian Cassa Depositi e Prestiti were not considered due to their characteristics as postal and pension banks.

Two dominant funding models stand out:

- Bond issuance – the main strategy for banks in China, Germany, and Korea.

- Loans from public funds – common in Japan and Brazil.

Bond issuance typically benefits from state guarantees and incentives, enabling low-cost market funding. Japanese banks, for example, combine both approaches, with a growing share of bonds alongside public loans.

BNDES: A Different Funding Model

BNDES differs significantly from its international peers. Bonds represent only a small portion of its liabilities: repurchase agreements (around 4,1%) and agribusiness (LCA) and financial bills—including development credit bills (1,5%).

Instead, BNDES relies heavily on transfers from the Workers’ Support Fund (FAT), which accounted for 53.3% of its resources in 2024 (under loans in the graph). While parafiscal funds exist in other banks, their weight is much greater in Brazil. Moreover, FAT’s cost is tied to the long-term interest rate (TLP), making BNDES’s funding structure more expensive than that of its peers.

Due to the expansion of FAT’s use by the BNDES and recent obstacles caused by major legislative changes regarding the fund’s management, the BNDES has been seeking alternative funding sources to complement its operations.

To diversify, the Bank began issuing LCDs in the domestic market in 2024. However, these securities:

- Lack explicit federal guarantees.

- Have costs close to market rates (historically high in Brazil).

- Are legally capped at 25% of the Bank’s equity, limiting their potential impact.

In 2024, LCDs represented 1.5% of BNDES’s funding, a proportion that rose to 2.0% in July 2025, totaling R$ 17.6 billion.

Why Is BNDES Different?

Several factors explain the BNDES’s unique funding structure:

- No explicit state guarantees for its own funding, unlike peers such as CDB, KfW, and KDB. Such guarantees enable, for example, high credit ratings from rating agencies, allowing low-cost funding.

- Mandatory dividend payments (25% of profits) to state entities, reducing equity growth.

- No tax exemptions.

- High domestic interest rates and economic volatility, making long-term funding costly.

These challenges underscore the need for greater state support and innovative funding strategies.

Green Bonds: The Future of Sustainable Funding

For most development banks, green bonds and sustainable bonds are the primary sources of green funding. These instruments combine environmental and social goals and benefit from state guarantees, enabling competitive rates.

For BNDES, resources from the Climate Fund play a similar role, even though they do not stem from direct bond issuance by the Bank. However, competing in international sustainable finance markets remains a challenge without explicit guarantees.

Funding from Green Bonds and the Climate Fund as a Share of Banks’ Liabilities (2024)

![Sources: Based on data from BNDES (2025a, 2025b), CDB (2025), KfW (2025), KDB (2025), DBJ ([202-]).](/.galleries/imagegallery/EE61_GRAF02.jpg)

Sources: Based on data from BNDES (2025a, 2025b), CDB (2025), KfW (2025), KDB (2025), DBJ ([202-]).

Among the five development banks analyzed, KfW leads the way in green bond issuance. With a stock of US$52.5 billion, green bonds account for 8.5% of its resources and are gaining importance, representing 15% of expected new funding for 2025.

Meanwhile, the Climate Fund represented 1.2% of BNDES’s funding in 2024, a share higher than the use of green bonds by CDB and KDB. By mid-2025, this figure rose to 2.8%, signaling the growing relevance of this type of funding for Brazil’s development bank.

Although BNDES issued an international green bond in 2017 and a domestic green financial bill (LFV) in 2020, these instruments did not become stable funding sources. The Brazilian Treasury began issuing sustainable bonds in 2023 under the Climate Fund framework.

The Global Sustainable Bond Market: Boom or Slowdown?

The green bond market—the first sustainable financial market—started in 2007 with the European Investment Bank’s inaugural issuance. It expanded significantly after the Paris Agreement in 2015, jumping from US$90 billion in 2016 to US$570 billion in 2021.

The global sustainable bond market finances a wide range of companies and activities, taking on risks that are very different from those assumed by development banks specifically.

However, global issuance slowed in 2022 and 2023, rebounded in 2024, but still remained below 2021 levels. This trend reflects:

- Interest rate hikes by the U.S. Federal Reserve, impacting global fixed-income markets.

- Skepticism about “green credentials” of issuers (Meng; Clements).

- Rising defaults on sustainable loans in 2022.

In early 2025, the outlook worsened. According to Sustainable Fitch, ESG bond issuance fell 25% in Q2 year-over-year, with green bonds down 32%. The decline is linked to:

- Geopolitical instability and trade tensions.

- High interest rates and tariff barriers.

- Policy reversals, such as the U.S. withdrawal from climate agreements and EU debates on relaxing corporate sustainability rules.

Bottom line: Short-term prospects for sustainable bond market growth are weak—even in historically committed regions like the EU.

Multilateral Banks: A Growing Force in Climate Finance

While sustainable bond markets face headwinds, multilateral development banks are expanding climate-related financing, especially for developing countries. These institutions offer credit lines and programs for climate projects and non-reimbursable resources in some cases. Partnerships with national development banks for green funding is an opportunity.

In June 2025, 70% of the BNDES’s external funding (R$ 24.5 billion) included contractual commitments to sustainable development.

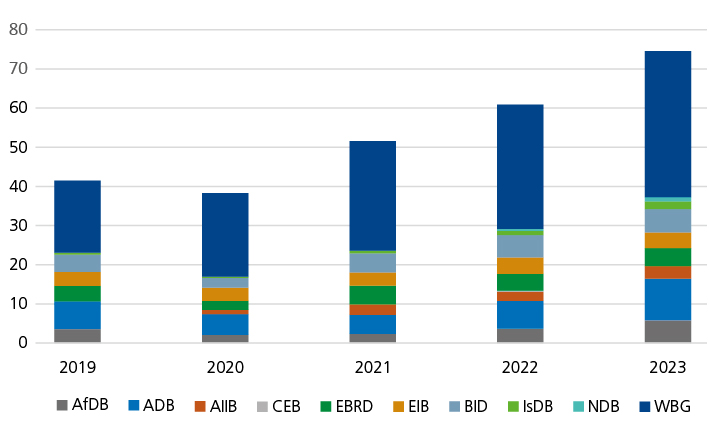

Climate Financing for Low- and Middle-Income Countries by Multilateral Organizations (US$ billions)

Source: Adapted from African Development Bank et al.

Note: AfDB: African Development Bank; ADB: Asian Development Bank; AIIB: Asian Infrastructure Investment Bank; CEB: Council of Europe Development Bank; EBRD: European Bank for Reconstruction and Development; EIB: European Investment Bank; IDB: Inter-American Development Bank; IsDB: Islamic Development Bank; NDB: New Development Bank; WBG: World Bank Group.

Multilateral banks have shown continuous and significant growth in financing climate-related activities, especially for developing countries. This trend differs from sustainable bond markets, as multilateral financing is less affected by U.S. interest rate dynamics.

However, recent geopolitical shifts—particularly the U.S. policy reversal on climate—may impact funding sources linked to U.S.-financed organizations such as the IDB and the World Bank.

Conversely, Asian multilateral development banks have expanded their role, increasing approved climate finance for low- and middle-income countries from US$ 6.7 billion in 2020 to US$ 15.9 billion in 2023.

Meanwhile, the Green Climate Fund, based in Songdo, South Korea, finances climate projects worldwide, having approved US$18.4 billion for such projects in various countries, sometimes in partnership with other development banks like KfW and the French Development Agency (AFD). BNDES is eligible to receive funding from this fund, although such operations have not yet occurred.

National development banks also invest in other countries, strengthening trade ties in priority areas often linked to sustainable development. Examples include BNDES’s relationships with KfW and AFD, banks that appear to continue prioritizing environmental agendas.

While trade and geopolitical tensions tend to increase risk and disrupt bond markets, relationships between national development banks may experience the opposite effect. New trade dynamics could create opportunities for funding among banks seeking to strengthen bilateral commercial ties, including in sustainable development.

What Does the Future Hold?

Despite the slowdown in sustainable bond markets, bilateral and multilateral partnerships may create new opportunities for green funding. Development banks in Europe and Asia continue to prioritize environmental agendas, even amid geopolitical uncertainty.

However, cuts in sustainability financing by major multilateral banks, especially those dependent on U.S. contributions, remain a significant risk.