BNDES Rural Credit and Land Concentration in Brazil: What You Need to Know

Brazil’s agricultural sector is one of the main engines of national development, positioning the country as the world’s leading net exporter of food.

BNDES Rural Credit and Land Concentration in Brazil: What You Need to Know

Brazil’s agricultural sector is one of the main engines of national development, positioning the country as the world’s leading net exporter of food.

In addition to technological development in the sector, which has enabled unprecedented scale in its activities, the country has consolidated, over time, an agricultural financing policy that involves public resources through rural credit.

But behind this success story lies a complex relationship between rural credit policies and land concentration—a topic that deserves attention.

Rural credit is the primary source of financing for Brazil’s agricultural sector, representing about 30% of the gross value of agricultural production. For the 2025–2026 crop year, more than R$ 500 billion were announced to fund activities such as operating costs, investments, and commercialization.

This credit is offered through institutions that are part of the National Rural Credit System (SNCR) that follow programs and lines of credit created by the Brazilian government and regulated by the Central Bank of Brazil. There are three main types:

Brazil faces high land concentration. According to IBGE:

The Gini index for land distribution in 2017 was 0.867, indicating extreme inequality—much higher than income inequality calculated through the Gini index.

This raises an important question: Does rural credit reinforce or reduce land concentration?

Producer size is typically correlated with the size of the rural property, so to assess the relationship between land concentration and rural credit, it is important to examine the profile of resource borrowers.

BNDES offers both subsidized and free credit. Since the Bank does not have branch offices, financing is carried out almost entirely through a network of accredited financial agents, who transfer the Bank’s resources to producers at the end point.

Source: Based on BCB data. Available at: https://www.bcb.gov.br/estabilidadefinanceira/tabelas-credito-rural-proagro.

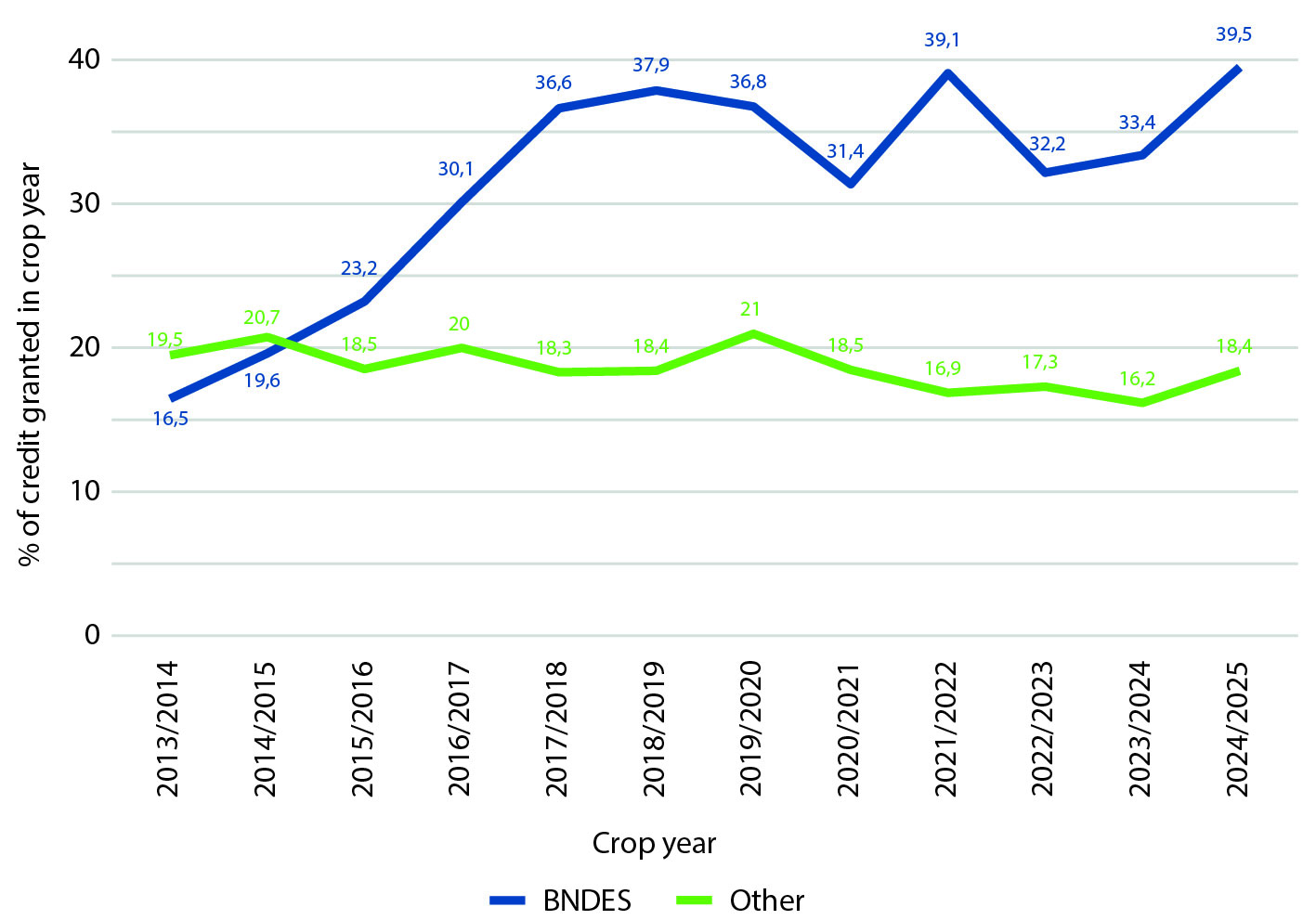

Recent data show a strategic shift by the BNDES:

The Bank focuses subsidized credit on small producers, mostly offering free and directed credit for bigger operations, of larger producers.

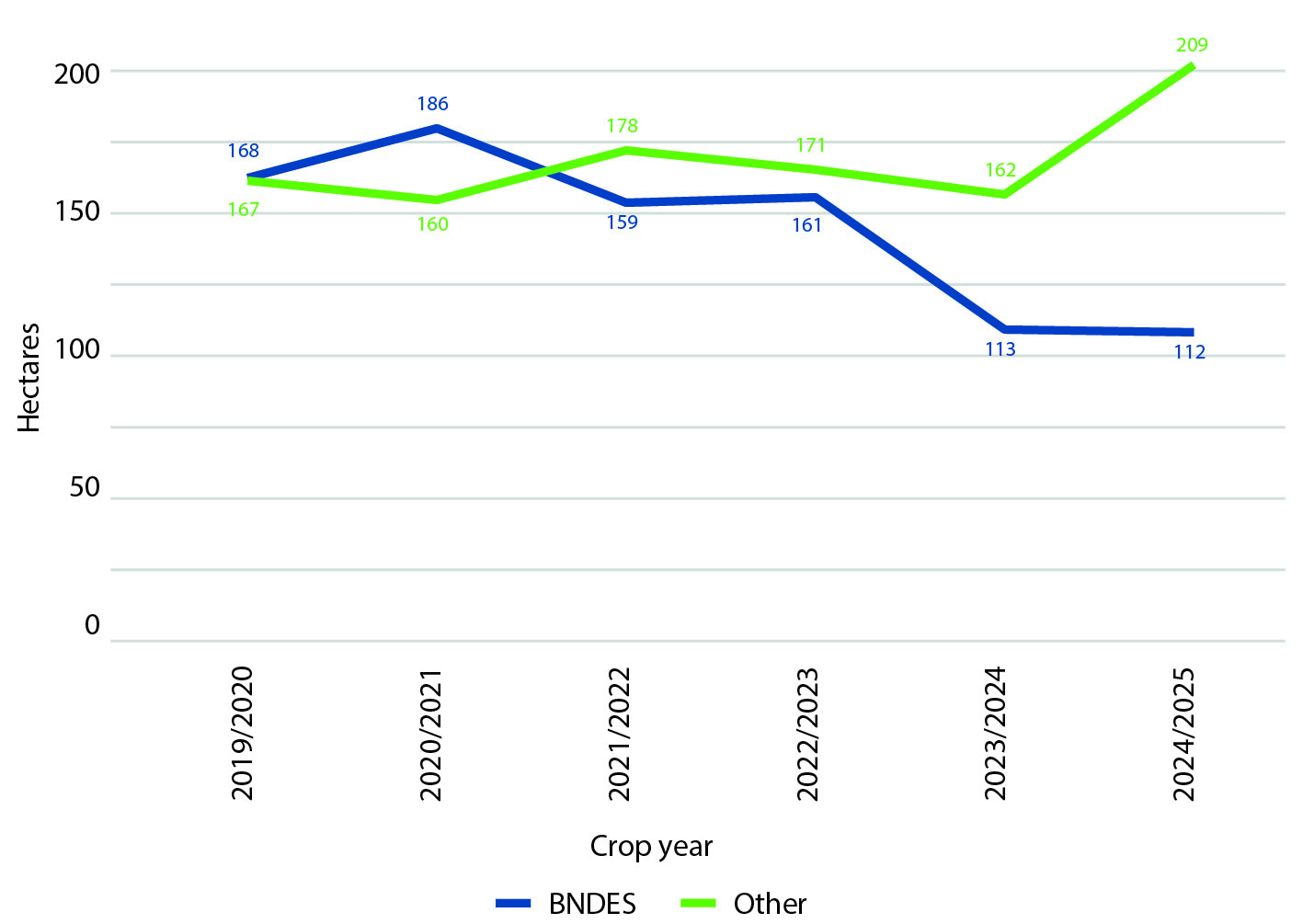

Moreover, the average property size financed by BNDES in 2024-2025 was 112 hectares, while the average property size financed by other institutions was 209 hectares, signaling a focus of the BNDES on smaller operations.

Source: Based on BCB (https://www.bcb.gov.br/estabilidadefinanceira/tabelas-credito-rural-proagro) and SFB (https://consultapublica.car.gov.br/publico/imoveis/index).

One key driver of this transformation is the rise of credit cooperatives:

This integration with the cooperative system allows BNDES to reach smaller producers and smaller areas, promoting inclusive growth.

By prioritizing small-scale agriculture, BNDES is not only fostering income and wealth equality but also potentially contributing to reducing land concentration—a structural challenge for Brazil’s development.

The relationship between rural credit and land concentration is complex and often debated. In this post, we’ll explore key hypotheses, evidence from BNDES, and what the data reveals about this dynamic.

Several hypotheses can be formulated about the link between agricultural credit and land concentration:

However, evidence suggests that credit primarily intensifies land use rather than expanding land holdings—especially for small and medium producers who have room to increase productivity without acquiring new land. This effect is strongest for investment credit from BNDES, indicating that more credit does not necessarily mean more land concentration.

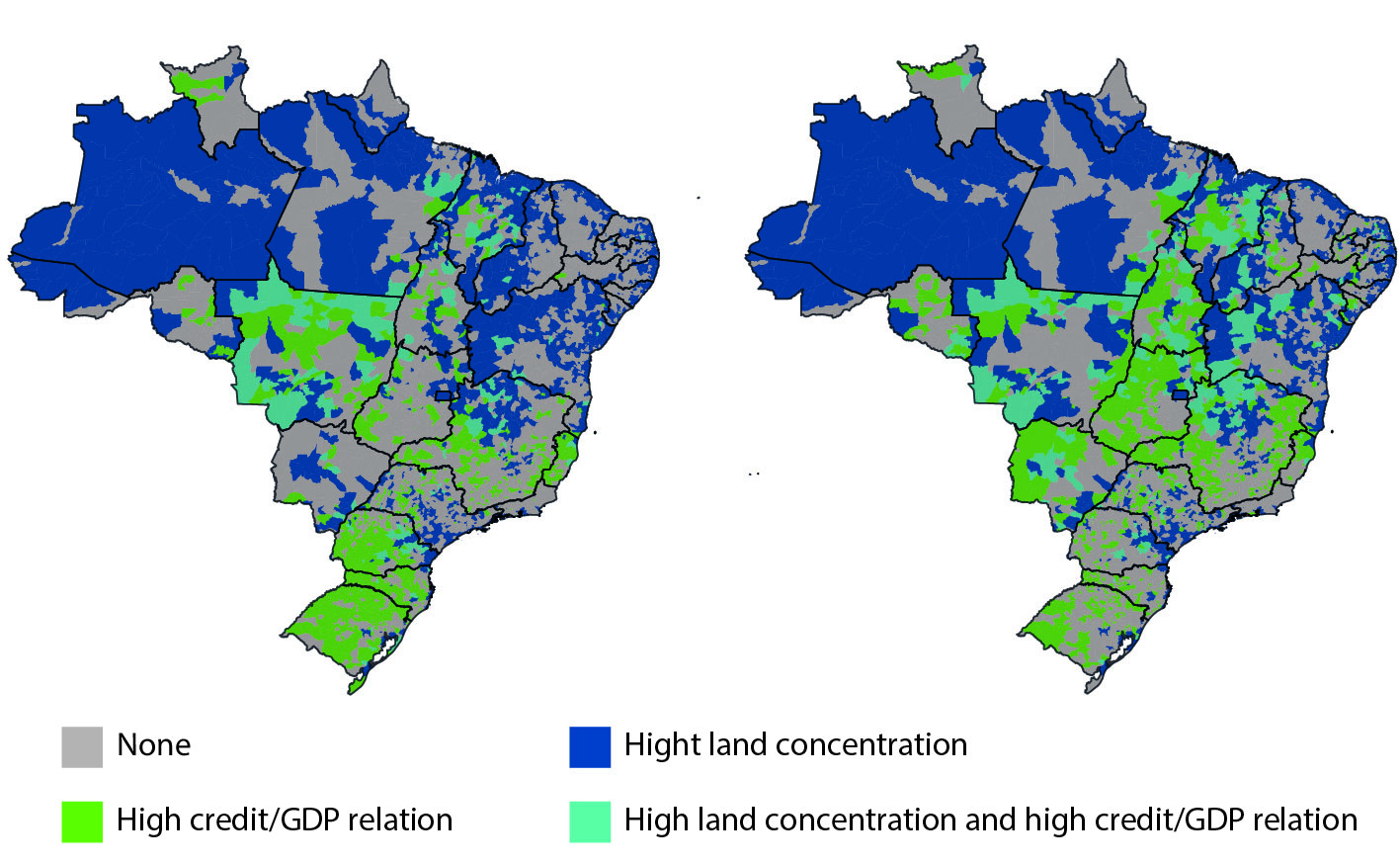

To understand this relationship, we compare BNDES credit with other financial institutions using two municipal-level indicators:

When mapping municipalities in the top quartile for both indicators, few areas show high rural credit/GDP ratios and high land concentration—except in parts of Mato Grosso, northern Minas Gerais, and the Northeast.

For BNDES credit, the disparity is even greater: its presence is strongest in the South, where properties are typically smaller. Other institutions show more overlap between high credit and high land concentration.

Source: Based on data from SFB (https://consultapublica.car.gov.br/publico/imoveis/index), BCB (https://www.bcb.gov.br/estabilidadefinanceira/micrrural) and IBGE (https://www.ibge.gov.br/estatisticas/economicas/contas-nacionais/9088-produto-interno-bruto-dos-municipios.html).

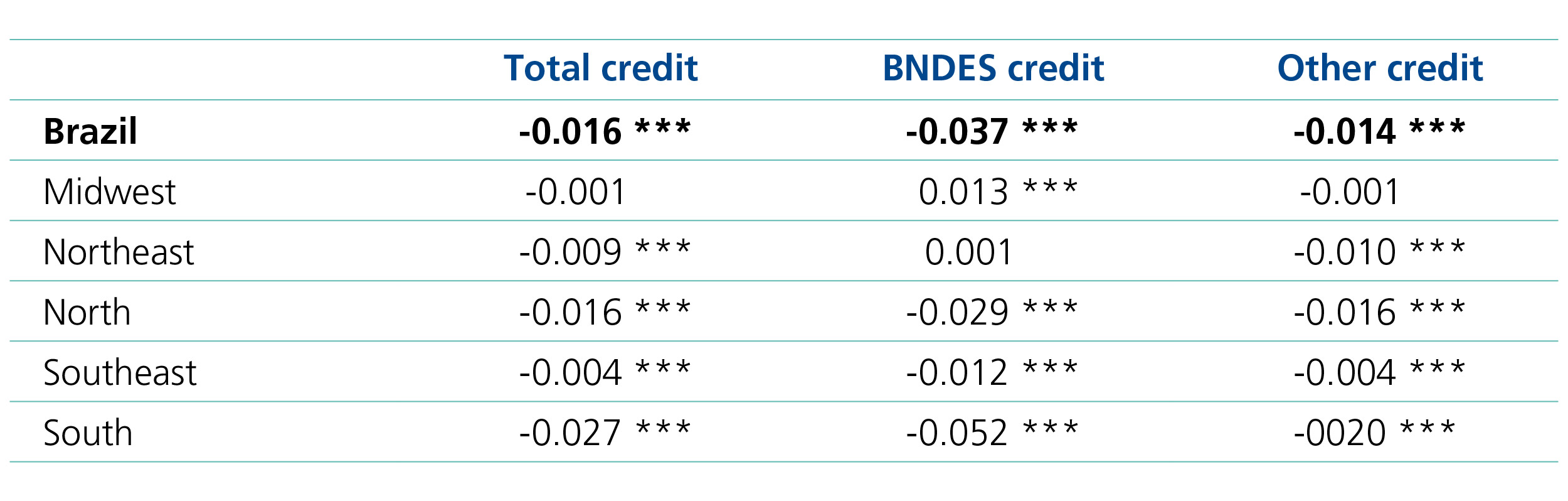

A simple linear regression at the municipal level reveals:

Source: Based on data from SFB (https://consultapublica.car.gov.br/publico/imoveis/index), BCB (https://www.bcb.gov.br/estabilidadefinanceira/micrrural) and IBGE (https://www.ibge.gov.br/estatisticas/economicas/contas-nacionais/9088-produto-interno-bruto-dos-municipios.html).

The negative correlation between BNDES credit and land concentration is stronger where credit flows through cooperatives. This reinforces the importance of cooperatives in promoting inclusive access to financing.

Source: Based on data from SFB (https://consultapublica.car.gov.br/publico/imoveis/index), BCB (https://www.bcb.gov.br/estabilidadefinanceira/micrrural) and IBGE (https://www.ibge.gov.br/estatisticas/economicas/contas-nacionais/9088-produto-interno-bruto-dos-municipios.html).

Although the data presented are indicative and require further analysis, the overall findings suggest that the Bank has played an important role in strengthening the sector without increasing land concentration, and highlight aspects that may help mitigate this phenomenon in financing operations carried out by BNDES.